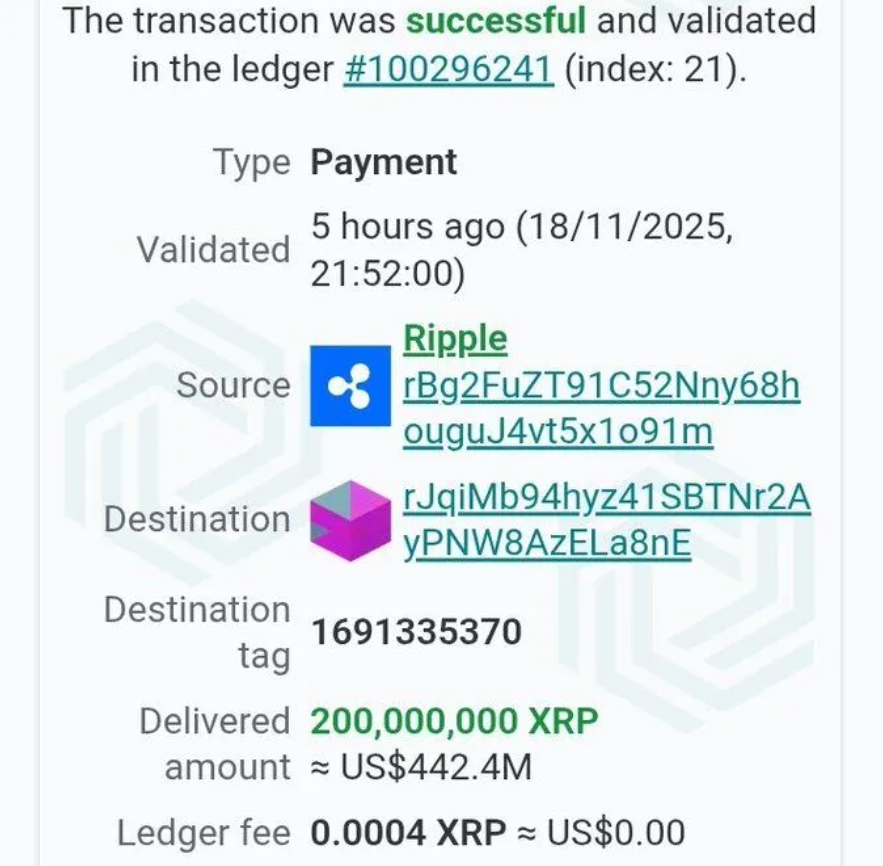

Ripple executed a transfer of roughly 200 million XRP, valued at about US$442.4 million, to a wallet active for approximately 12 years. The transaction involved an unusually low fee of just 0.0004 XRP.

The receiving wallet’s age and the size of the move have prompted speculation among analysts about Ripple’s treasury strategy, liquidity management or positioning ahead of broader adoption of its network.

Regulatory Guidance And Crypto Banking

In a related development, the US Office of the Comptroller of the Currency (OCC) has issued guidance that national banks may hold crypto-assets on their balance sheets specifically to pay blockchain network fees. That clarification removes a key regulatory barrier for banks engaging directly with public blockchains.

Because XRP was built for rapid, low-fee cross-border settlement on the XRP Ledger, this guidance could increase institutional interest in using it as a settlement asset or network-fee token.

Why Ripple’s Timing And Move Matter

The size of the transfer hints Ripple’s ability to move large volumes of XRP with negligible cost, demonstrating the operational attributes of the XRP Ledger compared with traditional banking rails.

At the same time, banks gaining permission to hold crypto for fees raises the possibility that networks like XRP’s could become more deeply embedded in banking infrastructure rather than remaining fringe assets.

This confluence of a large token movement and a regulatory shift suggests Ripple may be positioning its ledger not only as a token ecosystem but as an enterprise-grade settlement and fee infrastructure.

Strategic And Ecosystem Implications

Should banks begin holding crypto-assets for network-fee purposes, the role of tokens such as XRP could evolve from speculative assets to functional infrastructure components. That shift would require networks to demonstrate reliability, governance, auditability and integration with banking systems.

For Ripple the implications are significant: if its ledger is accepted in banking flows, the company may gain strategic advantage in the race for institutional on-chain settlement.

On the other hand, scrutiny will rise around large token transfers, wallet transparency and how treasury moves align with market and regulatory expectations.

What To Watch Next

Key indicators to watch include whether banks publicly adopt XRP or similar crypto-assets for network fees, how Ripple ties its wallet strategy to corporate disclosures, and how regulators monitor token flows in institutional contexts.

The behaviour of large-scale token transfers and how they are interpreted by markets and institutions will be central to understanding the next stage of blockchain-banking convergence.